401(k) Retirement Plan Advisors

A 401(k) retirement plan advisor educates and provides guidance to help participants in choosing the best plan for their needs and to improve chances of a successful retirement fund.

A 401(k) Plan is a qualified retirement plan in which an employer permits an employee to defer receipt of part of his or her compensation by contributing that part to his or her account in the 401(k) Plan. This is a paycheck deduction for the employee and is completely voluntary. Typically, a company will have a match of some sort as a benefit to the employees. The match is typically 50 cents on the dollar up to 6% of pay, thereby capping any potential match at 3% of payroll. The maximum payroll deduction for 2015 was $18,000 with a $6,000 catch-up provision for those ages 50+, and in 2016 the deferral limit is also $18,000 with the same catch-up amount.

The following is a table of 401(k) contribution limits:

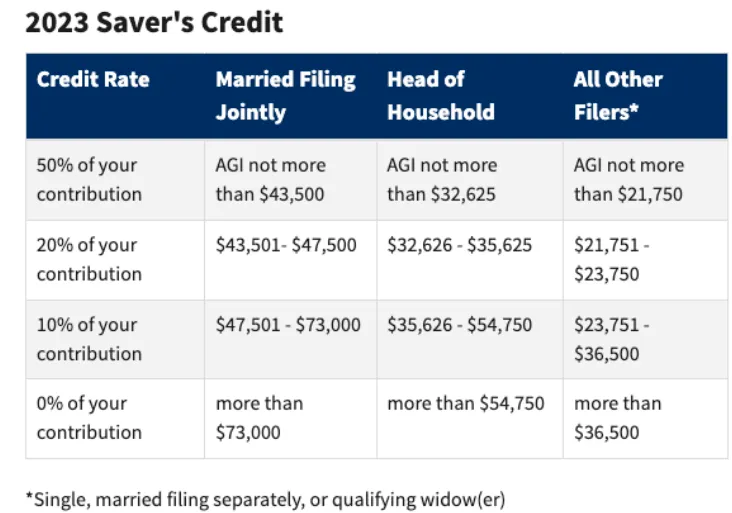

You may be able to take a tax credit for making eligible contributions to your IRA or employer-sponsored retirement plan. Also, you may be eligible for a credit for contributions to your Achieving a Better Life Experience (ABLE) account, if you’re the designated beneficiary.

Depending on your adjusted gross income reported on your Form 1040 series return, the amount of the credit is 50%, 20% or 10% of:

● contributions you make to a traditional or Roth IRA,

● elective salary deferral contributions to a 401(k), 403(b), governmental 457(b), SARSEP, or SIMPLE plan,

● voluntary after-tax employee contributions made to a qualified retirement plan (including the federal Thrift Savings Plan) or 403(b) plan,

● contributions to a 501(c)(18)(D) plan, or

● contributions made to an ABLE account for which you are the designated beneficiary (beginning in 2018)

401(k) Retirement Plan Advisors

We find that many people come to us because of the overwhelming quantity and conflicts in the financial industry. Most people do not have the time or interest to sort through it all and find the best solution for their needs. You can be confident that the 401(k) Financial Advisors at Full Focus Financial will put your needs first and will be proactive when it comes to saving you money. We will stay on top of and make sure to keep you informed of trends in the retirement plan industry, conduct vendor reviews and comparisons, and suggest changes based on new or updated laws. A 401(k) retirement plan advisor has the experience and training to make informed decisions for you.

If the following comment from your CPA sounds familiar to you, then your CPA is similar to most clients we talk with:

“Put money in your 401(k)/Profit Sharing Plan and pay taxes on the rest. If you want to take home more money, you need to make more money.”

We have found that very few CPAs are proactive when it comes to saving their clients money on taxes. Most CPAs simply process tax returns and are so busy that they do not have time to meet with individual clients to work on a true income tax reduction plan.

Are Qualified Plans Tax-Hostile or Tax-Favorable?

While most people think it’s a good idea to fund a “tax-deferred” qualified retirement plan; many times that’s NOT the case. In fact, tax-deductible qualified retirement plans can be more tax-hostile than tax-favorable.

You may have had someone ask you if it is better to pay taxes on the harvest or the seed? What this question is asking you is whether it is a better idea to pay income taxes now on your current income (the seed) if you could let that money grow tax-free and be removed tax-free later in retirement, or is it a better idea to let your money grow tax-deferred for year in a qualified retirement plan and then pay income taxes on ALL of the money that is withdrawn (the harvest).

We’ve run the numbers and for most clients under the age of 60, paying taxes on the seed while letting your money grow tax-free and come out of a wealth-building tool tax-free in retirement will be much better than simply income tax-deferring money the traditional way through a 401(k) or other tax-deferred qualified plan.

To learn how you can build a tax-favorable retirement nest egg outside of a qualified retirement plan, contact our 401(k) retirement plan advisors.

ADDRESSING 401(k) ISSUES

Protecting Your Employee's

Retirement From Mismanagement

Full Focus Financial is one of a few companies that focuses on the protection of employee sponsored retirement programs such as employee 401(k) accounts. For all companies large and small, we provide administrative services to ensure your employees retirement is protected and maximized. Full Focus Financial will provide each prospect (client) a customized Executive Summary, analyzing the Retirement Plan Performance, with the following information:

-Identify any Red Flags.

-Compare ratings for ROR & Fees with hundreds of like-sized companies.

-Estimated Savings available with reduced fees.

What Are the Benefits?

_Reduce Operational Drag

-Reduce Participant Fees

-Reduce Company Liability

-Put More Money into Pockets Of Employees

Full Focus Financial has expanded our team to be able to provide the services employees need at the thousands of companies that today have 401(k) programs that have been completely mismanaged. We are VERY concerned at the thousands of dollars lost by real people and real families on unnecessary fees and severely underperforming funds. We care too much about the fathers, mothers, and grandparents that are negatively affected to address this in half measure. We are reaching out to you so that you can secure a spot so that we can share with you EXACTLY what is going on at YOUR company in black and white and dollars and seconds since this information is available to the public.

We are confident we can reduce the overall plan cost by 32% – 65% AND take away 99% of the day-to-day management of the plan.

TESTIMONIALS

What others are saying

"Loved everything so far"

Working with Full Focus Financial has been a game changer for our business. Their expert guidance in managing our 401(k) plans has provided us with peace of mind and confidence in our retirement offerings. Their personalized approach ensures that every aspect—from compliance to employee engagement—is handled seamlessly. We highly recommend Full Focus Financial for anyone looking to optimize their 401(k) services.."

—Jennifer R., Satisfied Client

"My life changed forever"

Full Focus Financial has been an invaluable partner in helping us navigate the complexities of our 401(k) plans. Their deep industry knowledge, combined with a personalized approach, has empowered us to make informed decisions that align with our long-term financial goals. Their dedication to providing exceptional service and tailored solutions truly sets them apart. We couldn’t be happier with the results!."

—Michael T., Happy Customer

"Highly recommend this"

The team at Full Focus Financial truly cares about their clients. They went above and beyond to ensure I understood every step of my 401(k) planning process. Their professionalism and dedication are unmatched."

— Lisa M., Thrilled Client

We Have Time Slotted For You

Schedule An Appointment TODAY!

Our business is built on a foundation of thoughtful client relationships.

Contact Us

Retirement Plans

Privacy Policy

Terms of Service